Braes Paradox with Monetary Policies of the World’s Central Banks

The article discusses how the world’s major central banks are trying to use easy monetary policies in providing people with low-interest rates to encourage their customers to keep using their banks. The article states that although this policy has resulted in 32 trillion dollars that have gone into the global economy, because each bank is only considering their individual gains with this method, banks are actually straining the banking sector since bank equity prices have been dropping over the past few months.

I found that this concept relates to Braes Paradox and Nash Equilibrium. In a Nash Equilibrium, people have no incentive to change what they are doing, because there is no other option for them that will improve their situation. When there is a new option,( in this case lowered interest rates with certain central banks), everybody wants to switch over to this new option, because it will reduce their overall costs. People have an incentive to switch to these central banks because they will be less costly initially. However, in the long-run, if everybody switches over to this new option, conditions actually worsen for society in general which is the outcome of Braes Paradox. Because of this new option of reduced interest rates, these low and negative interest rates prompt investors to make riskier investments with collateralized loan obligations which are beginning to replicate what occurred in the 2008 financial crisis. This idea embodies that just because there is a new option that will make it better for people individually(and the individual banks), it doesn’t mean that those decisions will be good for society. In this case, the Nash Equilibrium does not maximize social welfare(the overall economy), which is why this is a huge problem for economic growth that will affect many countries around the world. The outcome of this situation is also similar to the outcome of the Prisoner’s Dilemma in that adding this additional new option of lowered interest rates will actually make it worse for the banks contributing to the economy long-term.

Because more people are trusting these banks and investors are making risky investments with their money, there is a lot more at stake and these people have the potential to lose a lot of money. In this new situation, there is no way, given the self-interested guided behaviour of customers to invest in these low-interest rate banks, for banks to get back to an even balance solution in which people equally use the low-interest rate banks and the high-interest rate banks.

Unless people stop becoming guided by their individual interests, it will be difficult to prevent the plummeting of the actual economy. However, I got to thinking of how this situation could have a solution that deviates from the Braes Paradox which could be helpful in alleviating this problem. Currently, with Braes Paradox, when the new option is added(banks providing reduced interest rates), since this is better than the old option(of banks with increased interest rates), all people have an incentive to switch over to the new option of banks with reduced interest rates. However, there could be a situation in which if everybody uses the new option(banks with lowered interest rates) suddenly the old option(banks with higher interest rates) becomes cheaper and people have an incentive to switch back. In this regard, I’m thinking that there should be some price in which if everybody decides to take the new option(lowered interest rate), then long-term this new option won’t be useful for all people because any one or so people will have the incentive to switch over to the old option of banks with increased interest rates because that would be more beneficial to them. I came to this conclusion by thinking how if everyone decides to use the cheaper interest rate, then its unlikely that that price will be the only cost banks will charge people since because banks want to be profitable and so they will find other ways to charge their customers using the low-interest rates(new option). It could be that some people have the incentive to switch from this new option of banks with lowered interest rates to the old option of other banks with higher interests rates because this new option would have other added costs that would end up making this new option costlier than the old option over time. This would allow an equilibrium to be formed in which some people use the banks providing the new option, while some people use the banks providing the old option.

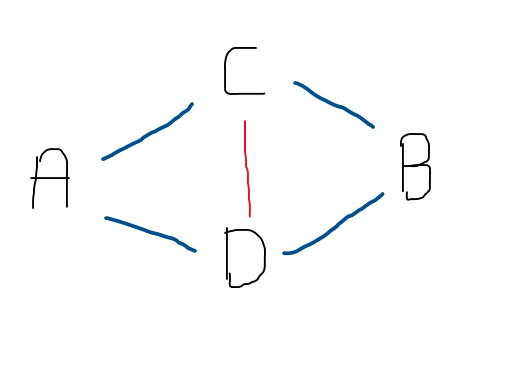

For example, in the figure below, let’s say that the original interest rate options were ACB and ADB. However, ACDB provided an interest rate that was lower than ACB and ADB. This would result in people having an incentive to switch from options ACB and ADB(old options) to ACDB(new option). However, it could be that not everybody has the incentive to switch to ACDB in the long-run because if everybody does so, it could be that the old options actually become cheaper than the new option because the old options have fewer additional bank costs. Then, finally, there would be an equilibrium in which all three “interest rate banking” options (ACB, ADB and ACDB) are used instead of just the one ACDB. Although this idea would be challenging and complicated to implement, I believe it could be something banks could consider incorporating to prevent future financial crises.

https://www.project-syndicate.org/commentary/monetary-policy-trap-travelers-dilemma-by-kaushik-basu-2017-10