Cascades with Consequences

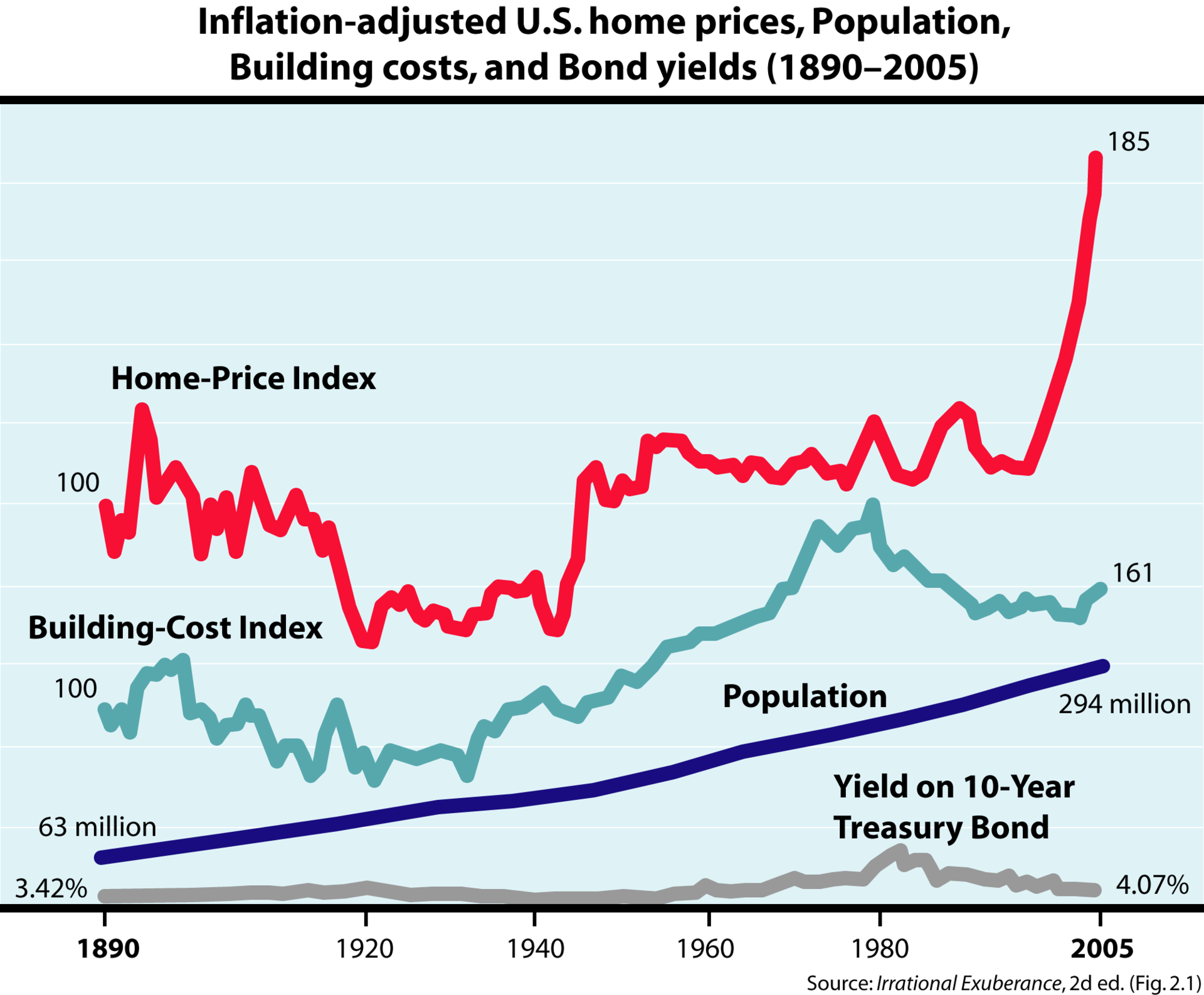

The recession from 2007-2009 has caused a lot of companies to go bankrupt, and for people to lose their jobs. What made this recession to occur was the housing bubble that started a few years before that. In early 2006, housing prices reached an all-time high in the United States, and then started to decline throughout 2006 and 2007, eventually bottoming out and reaching new lows in 2012.

In early 2006, housing prices reached an all-time high in the United States, and then started to decline throughout 2006 and 2007, eventually bottoming out and reaching new lows in 2012.

What caused this crash? A lot of the claims are that banks were giving mortgages to low-income neighborhoods, piling “subprime borrowers” (borrowers with low credit) with extreme amounts of debt, which eventually they couldn’t pay back and resulted in loans being defaulted on. While this is true, there can be a deeper level of analysis done on as to why so many people sold and bought subprime mortgages and loans, namely the effect of cascades.

Simple analysis can show that there were two sides of the causes of the crash — information based cascades and cascades based on direct benefit. The article I linked to says, “During the housing boom, there was a widespread belief that home prices could only go in one direction: up. If this were so, the risks of borrowing and lending against housing were negligible. Homebuyers could enjoy spacious new digs as their wealth grew. Lenders were protected. The collateral would always be worth more tomorrow than today. Borrowers who couldn’t make their payments could refinance on better terms or sell”. While very many people have little information as to how the housing markets work, and the risks of it, many people saw the allure of being able to get such cheap mortgages for homes, when they saw other people getting the loans. So many people abandoned their knowledge of housing markets (in this case, probably little knowledge as most people with low income and little experience of buying/selling houses), and followed the crowd. They assumed that if their neighbors were getting home loans, that they knew it was a good time to buy, and therefore abandoned their own information, trusting that their neighbors were doing the right thing.

The other side to this is the idea of cascades based on direct benefit. People benefit from buying homes when the economy is doing well. As long as people have jobs and everyone is prosperous, the value of housing only goes up, and so the investment of buying a house can easily return 20%, 30%, or more in a short amount of time.

What helps the economy to prosper and grow? People buying houses, and building new houses. As a result, as long as people were buying houses, the economy would do well, and so because of that it would be a direct benefit for oneself to buy a house and do well on that investment because of the economy.

On the other side, bankers had the information cascade of seeing others make thousands, millions, or even billions on these subprime loans, and they gave up their own information, believing that other bankers knew what they were doing.

All of these effects caused the housing market to boom, as shown in the graph above, and later, for it to eventually crash.

http://www.realclearpolitics.com/articles/2015/02/02/what_caused_the_housing_bubble_125463.html