Financial Takeovers and Auction Theory

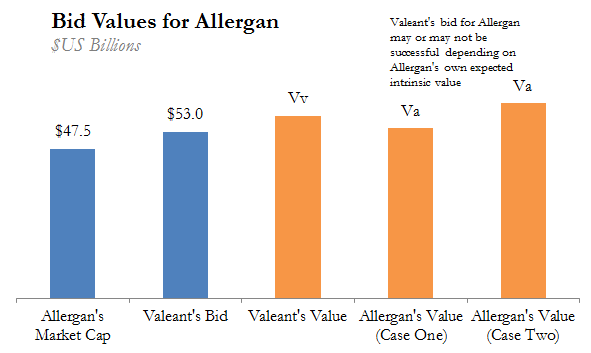

Perhaps the most heated corporate takeover battles currently is Valeant Pharmaceuticals’ attempted control of Allergan, the maker of Botox and other products. Over the past 5 months, Valent’s bid for Allergan has increased substantially from $45.7 billion to $53 billion, with bids all substantially above Allergan’s market capitalization at the time. In corporate finance mergers and acquisitions (M&A), an acquirer will always have to bid at a substantial premium to the target’s market value, and often make several bids in the process. This post will analyze why the M&A process works as such through the perspective of an ascending-bid auction by examining Valeant’s takeover attempt of Allergan..

In financial analysis, the way shareholders determines the intrinsic value of owning a company is by adding all future cash flows of a firm (discounted to the present) into perpetuity. Thus, both Valeant’s shareholders and management team have an idea of what the intrinsic value of Allergan will be. This value we will call Vv, or the value that Valeant places on Allergan. As we have seen in ascending-bid auction theory, the payoff that Valeant shareholders will receive is the difference between Valeant’s bid price (which we will refer to as Bv) and Vv. Valeant is thus willing to bid at prices above the current market capitalization (share price multiplied by shares outstanding) of Allergan so long as the bid is less than or equal to the intrinsic value Vv. The range of values can be seen in the chart below.

As Allergan’s management team, the key goal is to maximize shareholder value (in other words, increase stock price). Why, then, has Allergan not accepted Valeant’s bid, even though the latest bid of $53 billion is higher than Allergan’s market capitalization at the time of the bid ($47.5 billion) ? The answer is that Allergan’s management team (and shareholders) have their own intrinsic value of the company, denoted as Va, that is higher than Valeant’s latest bid. What’s interesting here is that Valeant doesn’t know what Va is, and whether or not Va is below Valeant’s intrinsic value of Allegan Vv. So while Allergan continues to deny Valeant’s ascending bids, Valeant can’t be sure whether its bid is still below Va, or if the bid has surpassed Va but Allergan’s management wishes to maximize the spread between Bv and Va on the deal. What’s certain is that once Valeant’s bid Bv has reached its estimation of the intrinsic value for Allergan at Vv, then it no longer makes sense to continue bidding. Thus, if and when Valeant makes a final bid for Allergan, market analysts would know that the bid value Bv is close to what Valeant estimates to be Allergan’s intrinsic value Vv.

Sources:

http://dealbook.nytimes.com/2014/06/10/allergan-rejects-valeants-53-billion-offer/?_php=true&_type=blogs&_r=0

http://www.valeant.com/about/valeant-allergan

http://online.wsj.com/articles/valeant-pushes-ahead-in-fight-for-allergan-1408924423